When the CDC’s eviction moratorium is lifted, 11 million Americans will face housing instability.

A housing complex in Albany County, New York on May 5, 2021. (Image: Tyler A. McNeil by Wikimedia Commons)

As many as 11 million Americans currently face eviction risk. On July 31, the Centers for Disease Control and Prevention will lift its 10-month eviction moratorium, permitting landlords to charge late fees, file for non-payment, and evict non-complying residents. For small landlords, this comes as a relief. For the approximately 14% of renters behind on housing payments, this presents a crisis.

“People generally extend themselves as far as possible in order to maintain their housing,” says Vincent Reina, associate professor in the Stuart Weitzman School of Design and the faculty director of the Housing Initiative at Penn. Reina studies urban economics, low-income housing policies, and community and economic development. According to his research, people cut back on food and utilities and defer medical treatment in order to come up with rent money. “That essentially means that people are putting as much of their wages as possible towards housing,” he says.

In Los Angeles, renters are most likely to reduce food consumption in order to make their rent.

Renters also borrow money, both from professional lenders as well as informally from family and friends, his research shows. These measures often buy renters a few more months of housing at the expense of compounding their debt as interest rates increase and causing credit ratings to plummet, decreasing their chances of securing future housing.

Reina studied this phenomenon in Philadelphia, looking at the pandemic’s impact on housing.

“For tenants who manage to stay housed even as their back rent accumulates, the debt may become too large to pay off, even if the economy were to fully recover,” he and colleagues wrote in a research brief. “On the other hand, if landlords cannot collect rent, their ability to meet their own financial obligations is impaired.”

“We’re at a moment where there’s a perfect storm, in many ways,” Reina says. The federal eviction moratorium was enacted in order to reduce the spread of COVID-19, but there was a lag in federal response, which means that “now we’re trying to ramp up efforts at the same time as the moratorium expired,” he says.

For many Americans, affordable housing is out of reach. A bullish real estate market and supply costs have driven up property values in many cities, he says, and the rate of new construction has slowed. “An inadequate development of new units essentially decreases the overall supply of available units and therefore increases price over time,” he says.

In places with high vacancy rates like Philadelphia there are chronic issues around housing quality and the cost of maintenance. Maintaining a decent, quality, affordable home takes time and money, Reina says. “That, to be honest when you actually work out the math, often exceeds people’s income and ability to pay. So, there’s often a challenge on both ends, both in the production but then also the preservation of units over time.”

The National Income Housing Coalition points to the wage gap right around minimum wage, which is insufficient to secure the average housing unit in many markets, Reina says. “Many subsidized households are people who are essentially the working poor,” he says. His research also shows that, increasingly, this also includes elderly households that have aged out of employment. Older individuals who have earned lower incomes over the years are being exposed to a financial shock just as they enter retirement. “There’s no way to bridge that gap going forward,” Reina says. “I think the current pandemic also shows that though there are a lot of shocks that households face right now, natural disasters and global health pandemics could essentially push someone over the edge.”

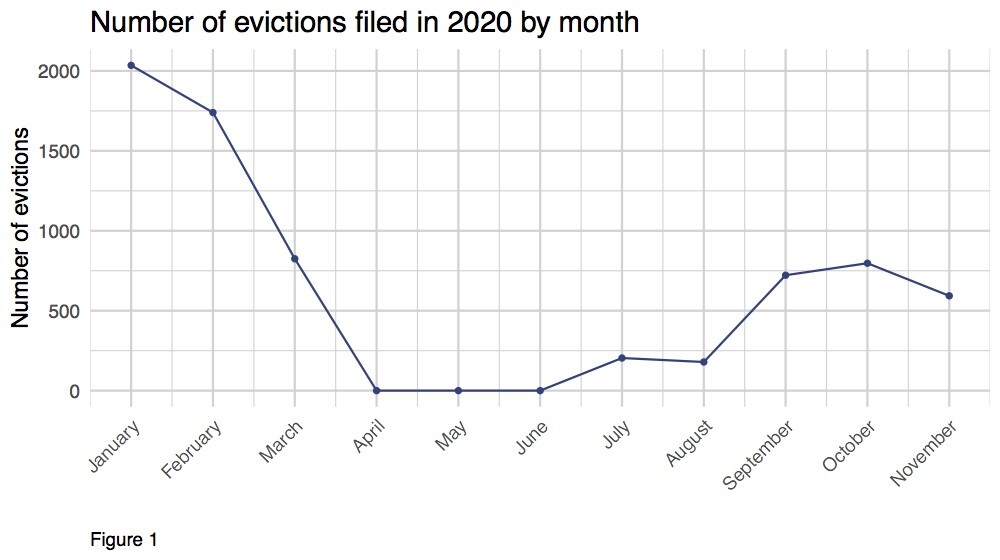

Evictions drastically decreased as a result of the CDC moratorium.

The last year has shown interesting innovation on the local and national levels, showing a broad set of solutions being offered, which Reina would like to continue to see. “There’s no one set policy that will solve everything,” he says. “We really need to learn from innovation and kind of try to incorporate that into our into our thinking going forward.

“My hope over the next five years is that we don’t see the current investment the federal government’s making with respect to the pandemic as something that should just go away,” Reina says. “We need to see a more robust commitment from the federal government to acknowledge the essential role that housing plays in our health, our overall well-being, and for our society more broadly.”

The federal government should not define housing markets nor should it be the only entity providing solutions, but it is essential to ensure that housing affordability challenges are meaningfully addressed, Reina says.

The CDC recently extended their eviction moratorium from June 30 to July 31. Reina’s work was cited in the extension document regarding the impact of emergency rental assistance funds on eviction prevention.

Novel plant-based approach to a better, cheaper GLP-1 delivery system

Research led by Penn Dental’s Henry Daniell investigates the use of a lettuce-based, plant-encapsulated delivery platform as a new oral delivery of two GLP-1 drugs previously approved by the FDA in injectable form.

No brain, no gain: Neuronal activity enhances benefits of exercise

Research led by Penn neuroscientist J. Nicholas Betley and collaborators finds that hypothalamic neurons are essential for translating physical exertion into endurance, potentially opening the door to exercise-mimicking therapies.

In honor of Valentine's Day, and as a way of fostering community in her Shakespeare in Love course, Becky Friedman took her students to the University Club for lunch one class period. They talked about the movie "Shakespeare in Love," as part of a broader conversation on how Shakespeare's works are adapted.

In Becky Friedman’s English course Shakespeare in Love, undergraduate students analyze language, genre, and adaptation in the Bard’s plays through the lens of love.

Beating the heat: Designing cooling for bodies in motion

Dorit Aviv, director of Weitzman’s Thermal Architecture Lab, studies how humans, technology, and design intersect, paving the way for the development of novel approaches to cooling people efficiently.

{kind=link}

{kind=link}